Don’t Let Mortgage Debt Headlines Fool You

You may have seen the headlines lately about mortgage debt in America hitting a record high. Maybe your brother-in-law brought it up at the dinner table last weekend, dropping the statistic like he was warning everyone about an incoming financial meteor.

Here’s the thing: He’s not wrong about the number. But he only has half the story. And the half he’s missing? It changes absolutely everything.

While big scary numbers make for great news alerts, homeowners are actually sitting on some of the strongest financial footing we've seen in decades. Let's look at the actual data to see why today's housing market is built on a rock-solid foundation—not a house of cards.

The Headline Number Is Real, But It’s Missing Context

Yes, according to data from the Federal Reserve, outstanding U.S. mortgage debt sits at an all-time high of roughly $14.4 trillion. When you pair that number with everyday stories about inflation and budgeting, it's incredibly easy to assume we are staring down a repeat of 2008.

But looking at debt without looking at total property value is like looking at a business's expenses without checking its revenue. To see the true health of American households, we have to look at the balance sheet as a whole.

Right now, total U.S. home values sit at an incredible $47.9 trillion. Out of that massive total, homeowner equity accounts for $34.1 trillion—which represents the share of the homes that owners actually own free and clear. The remaining $14.4 trillion is the collective mortgage debt everyone is worried about.

The math tells a completely different story than the headlines. The equity homeowners have built up is more than double the amount of debt they owe.

Why This Is Opposite of 2008

Think back to the years leading up to the 2008 crash. During that era, the line tracking aggregate mortgage debt actually climbed higher than the equity people held. Homeowners had virtually no cushion. When home prices experienced a drop, millions of people instantly fell "underwater," owing more than their properties were worth.

Today, the gap between what people owe and what they own is at a historic wide. Because homeowners have so much skin in the game, the risk of a systemic wave of foreclosures is incredibly low.

Most Homeowners Are in a Rock-Solid Position

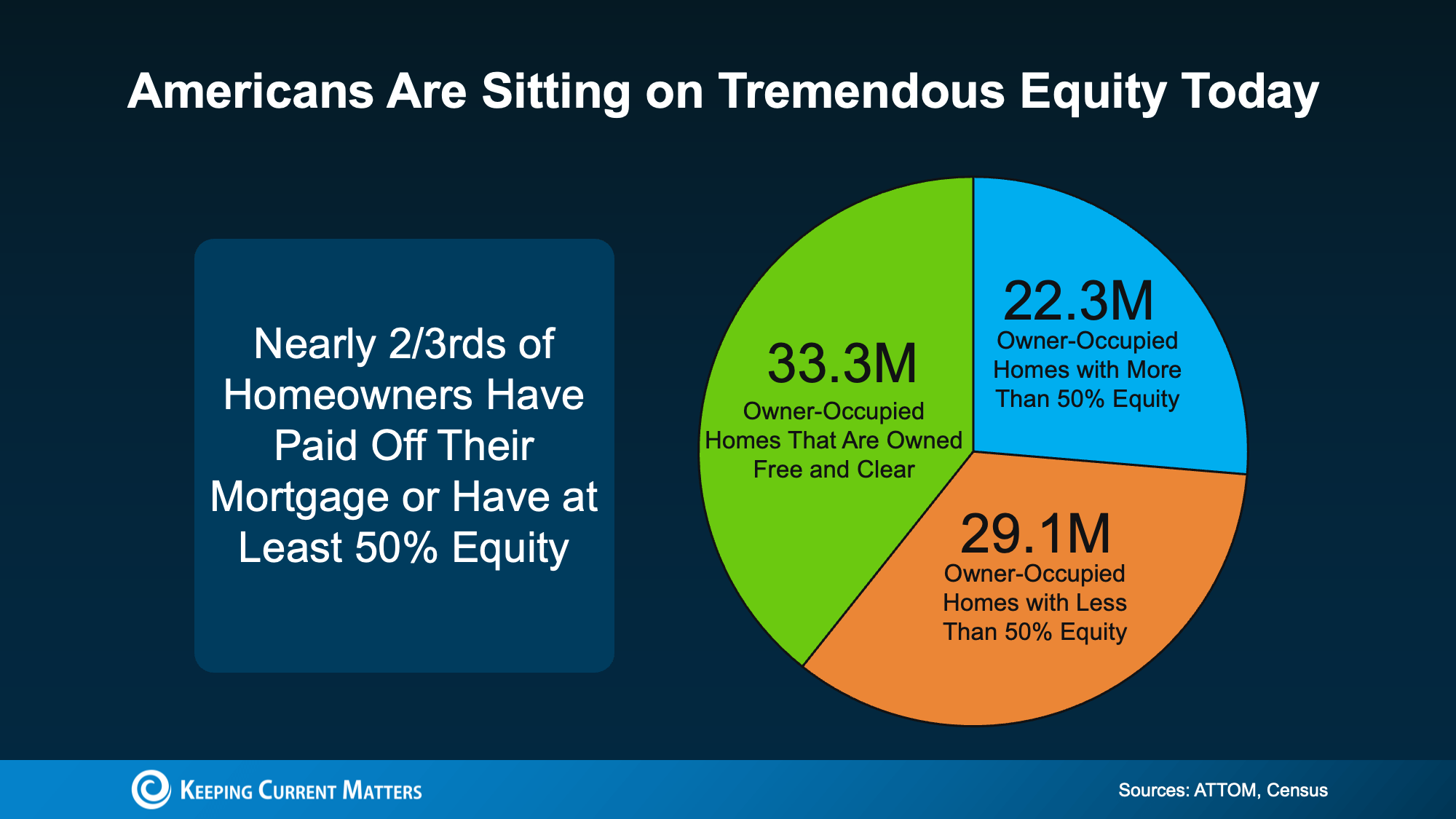

We know that equity is massive on a national level, but what does it look like when you break it down by individual households?

According to data compiled from ATTOM and the U.S. Census Bureau, American homeowners generally fall into three distinct buckets, and two of them are remarkably stable:

When you add the first two categories together, nearly two-thirds of all American homeowners have either completely paid off their mortgage or hold an equity stake greater than 50%.

The Bottom Line

Record mortgage debt sounds alarming on a cable news scroll. But when it's backed by near-record home values, tight lending standards, and historic levels of household equity, it represents growth—not instability. The brittle conditions that triggered the Great Recession simply do not exist in today's landscape.

The market isn't teetering on a ledge; it's anchored by millions of homeowners who are more financially secure than ever.

What does this mean for your neighborhood?

If you're trying to figure out how these national numbers translate to your neck of the woods—whether you are looking to tap into your equity, buy your first home, or simply time a move—let's chat. Send over a message anytime for a data-driven look at your local market. No pressure, just clear answers.